LCL Consolidation in Singapore: How Independent Forwarders Can Compete on Price Without Sacrificing Margin

LCL is one of the most competitive corners of freight forwarding, and Singapore is where that competition is most intense. The world's four biggest co-loaders operate here. The largest MNCs in the industry run weekly lanes out of PSA terminals. And every independent forwarder trying to win LCL business from the same shippers is quoting against rates that those players can sustain because of sheer volume.

The good news: volume is not the only way to compete. The right approach to consolidator relationships, pricing structure, and a strong freight forwarder network in Singapore can give independent operators a real edge without racing to the bottom on margin. This post breaks down exactly how.

Why Singapore Is Still the LCL Hub That Matters

Before getting into the margin mechanics, it helps to understand why Singapore remains the market that forwarders need to be serious about.

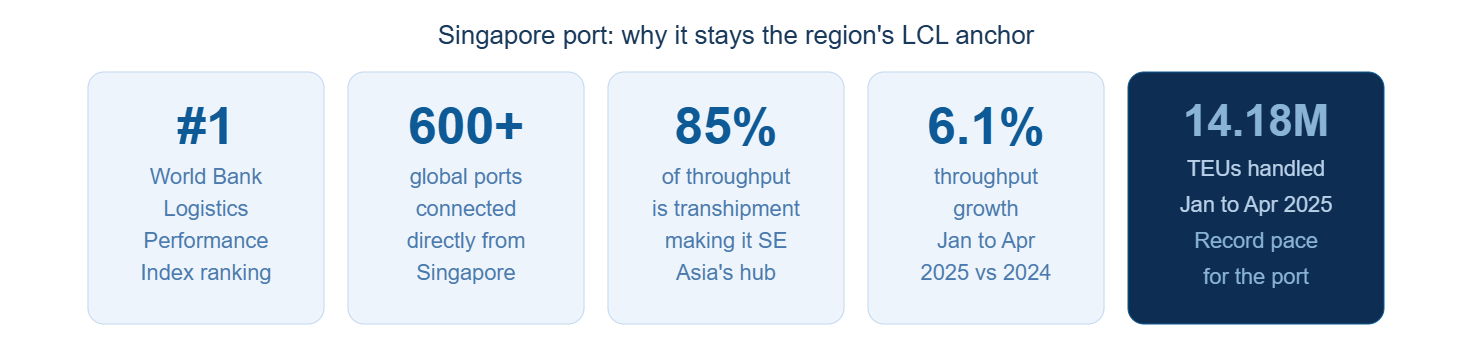

Singapore Port is ranked number one globally in the World Bank Logistics Performance Index and its massive network connects to over 600 global ports. Transhipment operations represent 85% of Singapore's container throughput, confirming its role as Southeast Asia's primary redistribution centre. Between January and April 2025, container throughput reached 14.18 million TEUs, reflecting a strong 6.1% increase over the same period in 2024.

The Tuas Mega Port expansion reinforces all of this. It is not just a capacity increase. It is a digital and automation overhaul that will make Singapore's handling more efficient and its advantage over competing regional hubs harder to close.

For independent forwarders, this is both the opportunity and the problem. The volume flowing through Singapore is enormous. The competition for a piece of it is equally enormous. Knowing how LCL margins actually work is the prerequisite for playing in this market without bleeding out on price.

How LCL Margins Are Structured, and Where They Disappear

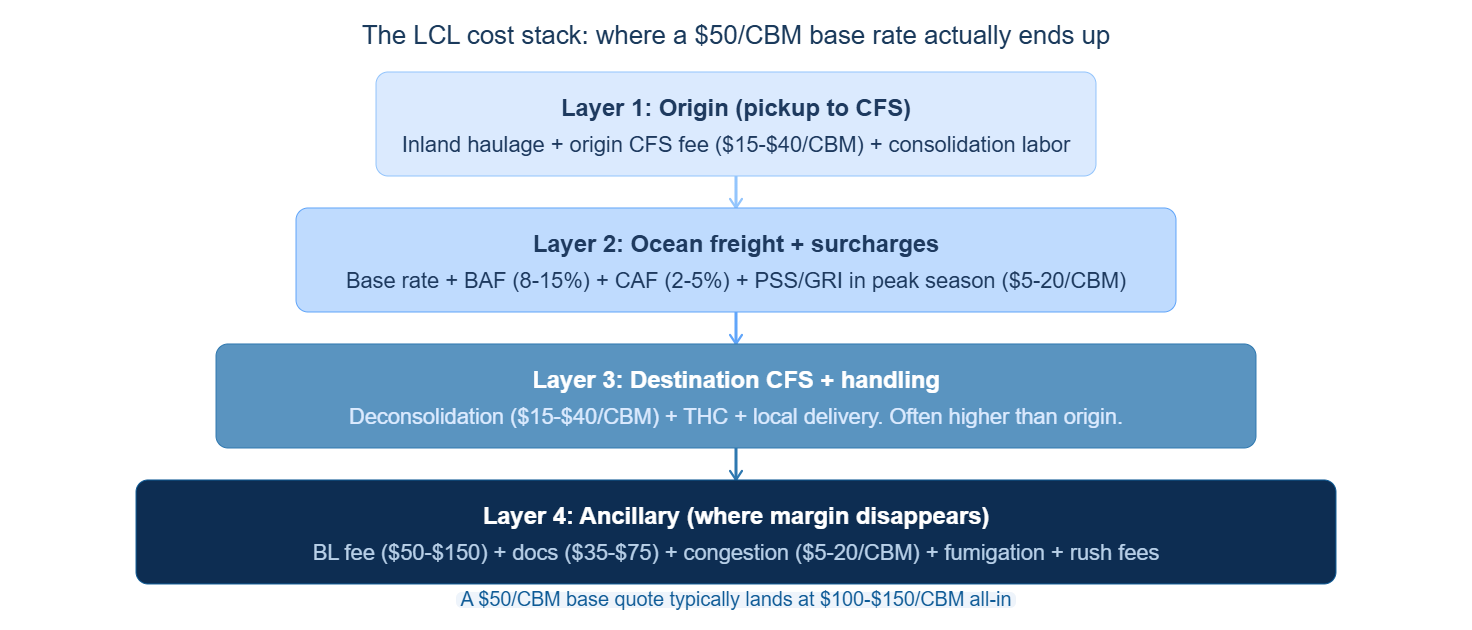

The pricing structure of LCL freight is layered in a way that makes it easy to win the quote and lose the margin at the same time. Here is how the cost stack actually works:

LCL quotes can look like alphabet soup: CFS, THC, BAF, CAF, PSS, GRI, EBS, and more. A "$50/CBM base" typically becomes $100 to $150/CBM all-in. The forwarder who quotes the lowest headline rate and then passes through all four cost layers without discipline ends up in two bad places: either the shipper sees the all-in number and walks, or the forwarder absorbs the difference and bleeds margin.

The destination layer is where most independent forwarders lose control. One of the most profitable ways to make a margin from an LCL shipment in this region is to stack the margin at the destination port. That is exactly what the MNCs and large consolidators do. Independent forwarders who do not have a strong partner at the destination pay full rack rates on deconsolidation and handling, effectively handing margin over to the destination agent.

This is the structural problem. And it is also the structural solution, because the forwarder with a strong, trusted partner at the destination is the one who controls both ends.

The Four Consolidators Who Dominate This Market

Before independent forwarders can compete effectively, they need to understand who is actually running the boxes.

The global LCL market is dominated by four global players, also known as co-loaders or consolidators: Vanguard Logistics, Shipco, ECU Worldwide, and CWT Globelink. The bulk of their customer base comes from the overflow volumes cascaded down from the top 50 global forwarders, and the rest comes from local forwarders. They are considered neutral because they support the cargo of multiple forwarder competitors in the same consolidation boxes, and they do not go after the retail shipper market.

This neutrality is the key insight for independent forwarders. The co-loaders are not your competition. They are your infrastructure. The question is whether you are accessing their boxes on terms that allow you to make money, or terms that mean the co-loader makes all the margin and you make the relationship.

The challenge for any consolidator in building any new LCL trade lane between two port pairs is getting a baseload volume or anchor customer. Baseload volume is shipment volume that a forwarder or consolidator can rely on through thick and thin to arrive at the CFS for loading on a daily or weekly basis. The easiest way to do this is to focus on clients that can offer stable, regular volumes on a certain port pair and to get them committed to long-term contracts at below-market rates.

This is exactly the leverage point independent forwarders can use, provided they can aggregate volume. A forwarder moving 50 CBM a month on a lane has more negotiating power than they often realise. A forwarder whose network can commit 200 CBM across several members has meaningful rate access.

Five Practical Ways Independent Forwarders Protect Margin

1. Quote all-in from the start

The most common margin leak in LCL is quoting a competitive per-CBM rate and then absorbing destination charges that were not factored in. Some suppliers quote low CIF, but the destination agent inflates charges, with destination fees reported at 2 to 5 times higher than expected. Always request a full cost breakdown before shipment.

Independent forwarders who price all-in from the first quote eliminate the surprise conversation later. Yes, the headline number looks higher. But shippers who have been burned by hidden destination fees will trust the transparent quote over the low teaser rate. Margin protection starts with quoting honestly.

2. Know your FCL break-even point and tell clients

When your shipment passes roughly 12 to 15 CBM, FCL often becomes cheaper on a per-unit basis than LCL, especially once you factor in local charges and time. Independent forwarders who proactively advise clients on this threshold position themselves as trusted consultants rather than rate vendors. The client gets better economics. The forwarder wins loyalty that survives rate comparisons.

3. Build volume on your core lanes, not everywhere

One way to build a profitable trade lane is to concentrate spending on key carriers and focus on high-margin clients, but there are trade-offs to balance: higher-paying cargo usually comes at the expense of volume, and high volume at the expense of high margins.

Independent forwarders who try to compete on every Singapore lane spread their volume too thin to negotiate anything. The ones who pick two or three lanes they understand deeply, build consistent weekly or monthly volume, and lock in contract rates with their consolidator earn the rate differential that makes quoting at competitive prices sustainable.

Shippers who commit to 50 or more CBM annually can negotiate rates 15 to 25% below the spot market. Consolidators who commit to 200 or more CBM get even better rates.

4. Control both ends of the shipment

The destination CFS is where independent forwarders pay the highest rack rates and have the least visibility. Some forwarders offer negative freight rates at the origin port to the shipper, then collect the amount back from their destination office, which in turn collects it from the consignee. The market pricing ends up with very lopsided charges and overwhelming costs back-loaded in destination markets.

Forwarders who have a strong, vetted partner at the destination can negotiate destination handling rates in advance, pass a better all-in price to the shipper, and keep the margin that would otherwise disappear into an unknown agent's fee structure. This is one of the clearest advantages that comes from being part of a freight forwarder network in Singapore with members at both ends of every lane.

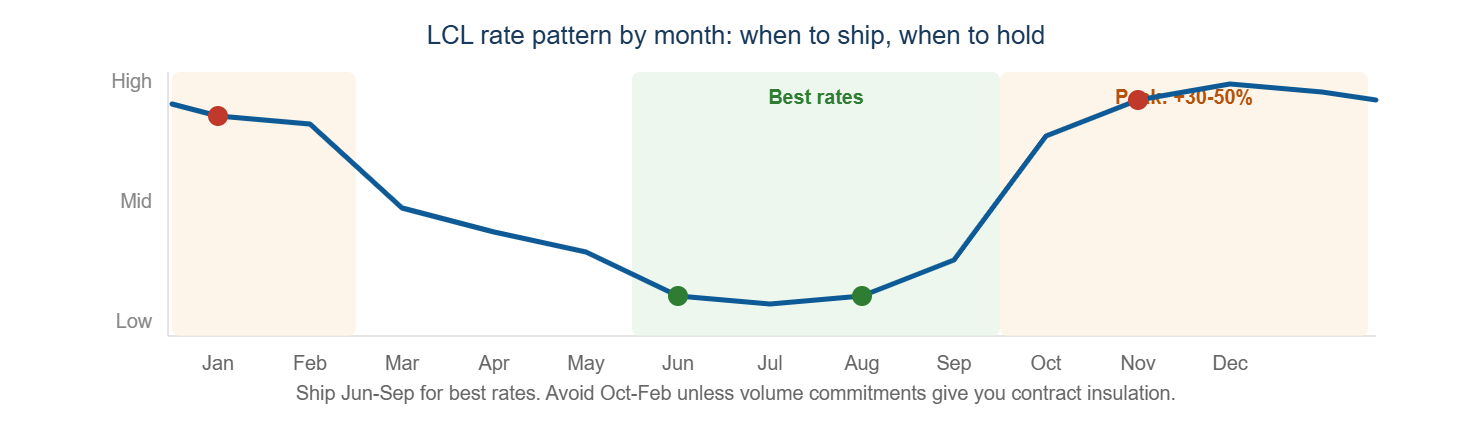

5. Time the market: avoid peak season rate spikes

June through September typically offers the lowest LCL rates. Avoid Q4 (October to December) and January to February, when rates spike 30 to 50% due to peak seasonal demand. Independent forwarders who understand their clients' inventory cycles and plan shipments around rate windows can build in a margin that is simply not available to forwarders who quote reactively.

The Seasonal Rate Pattern Every Singapore Forwarder Should Know

The pattern is consistent year on year. Forwarders who can help clients plan inventory cycles around the rate calendar provide a genuine service that goes beyond finding the cheapest box. Clients who follow this advice save money. Forwarders who enable that saving earn relationships that hold through competitive tendering.

Where Network Membership Changes the Equation

This is where the structural advantage of being part of a freight forwarder network in Singapore with global reach becomes practical rather than theoretical.

Independent forwarders face three problems in LCL that network membership directly addresses:

Volume to negotiate with. A single forwarder moving 30 CBM a month on Singapore to Rotterdam cannot get a contract rate. A network of forwarders who agree to pool their volumes on that lane and present it to the co-loader as a committed block absolutely can. Forwarders with high LCL volumes get better rates from consolidators. The network creates that volume without requiring any individual member to take on cargo they cannot fill.

A trusted partner at destination. The margin leak at destination CFS is only solvable if you know exactly who is handling your cargo and what they will charge. Within a vetted network of freight forwarders, the destination partner is already screened for service quality, financial stability, and professional standards. That is precisely how X2 Logistics Networks approaches membership: quality over quantity, with partners who have been assessed before they join the group.

The ability to compete with MNCs on coverage. Singapore's superior feeder density minimizes waiting time and storage costs, providing a structural advantage over competing direct consolidation services, which are only viable for the largest, high-volume routes. Independent forwarders who can demonstrate the same geographic coverage through their network partners can offer shippers the reliability of a global operator without the overhead of a global operator.

X2 Logistics Networks promotes cooperation and enhanced business growth for members actively seeking mutually beneficial opportunities founded on trust. Members maintain a high degree of business ethics and respect for their clientele and fellow members. In LCL specifically, that trust is not soft language. It is the mechanism by which forwarders at both origin and destination exchange cargo, share rate intelligence, and build the volume commitments that unlock competitive pricing.

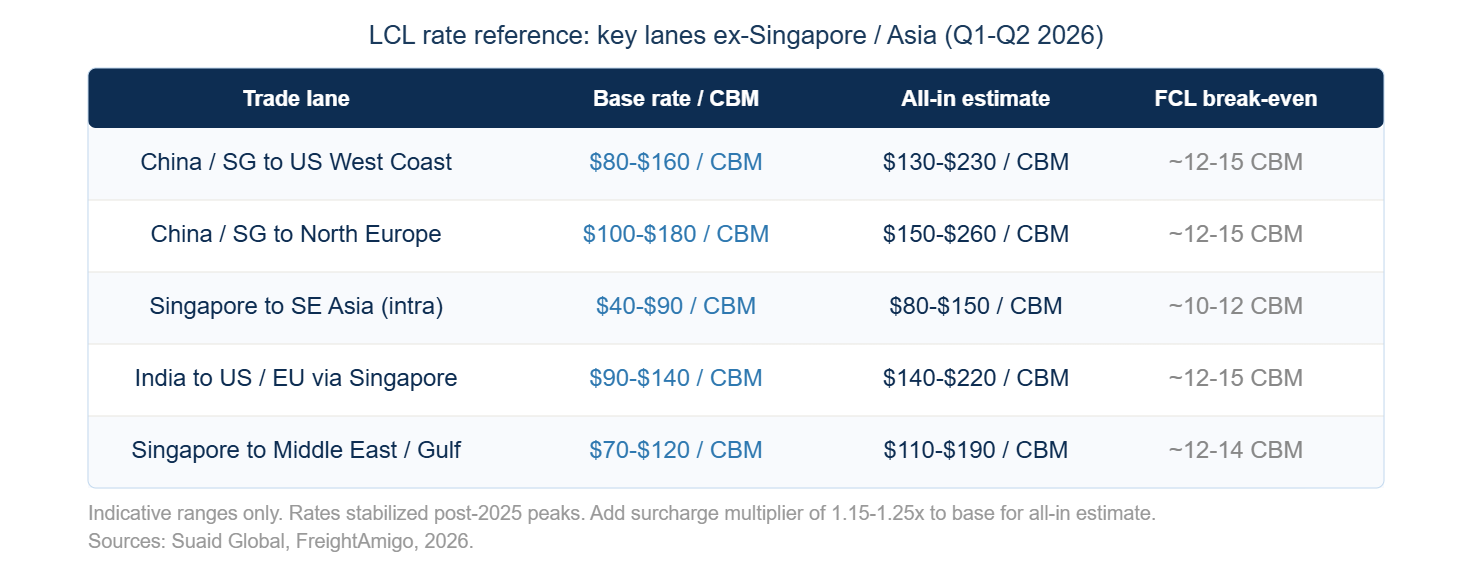

LCL Pricing Reference: What Forwarders Are Working With in 2026

As of April 2026, LCL rates have stabilized post-2025 peaks, influenced by vessel overcapacity and modest 1.7% global trade growth. Stable rates are good news for forwarders building volume commitments on core lanes, because the co-loaders are more receptive to contract conversations when the spot market is not running hot. This is the window to lock in rate structures that will protect margin when peak season arrives.

FAQ: What Independent Forwarders Ask About LCL in Singapore

How do I compete with MNCs on LCL price when they have far more volume than I do?

You do not compete with them on total volume. You compete on lane focus, relationship quality, and service at both ends. An MNC routing LCL through Singapore on 40 lanes simultaneously is spread across consolidation relationships that are managed by systems, not people. An independent forwarder who knows three lanes exceptionally well, has a trusted partner at destination, and quotes all-in from day one is a more reliable operator for a mid-size shipper than a global giant's online booking portal. That is the pitch. Be specific about what you actually do well.

What is co-loading and when does it make sense?

Co-loading is when a forwarder who cannot fill a consolidation box on their own feeds their cargo to a neutral co-loader who combines it with cargo from other forwarders heading to the same destination. Big forwarders mainly run gateway models where they route cargo from the region into a major port hub and then re-export it out to the final destination. For independent forwarders, co-loading is the access point to lanes where they do not have enough weekly volume to run their own box. The margin question is about what rate you negotiate with the co-loader versus what you charge the shipper.

What happens to my cargo if another shipment in the same LCL box gets held at customs?

If any shipment in the shared container triggers an inspection, everyone in that box can be delayed. Examination, storage, and handling fees are often split between all consignees. This is one of the less-discussed risks of LCL. Always ask your consolidator how DG and inspection risk is managed across the box. Better co-loaders have procedures for separating inspection-risk cargo. And always get cargo insurance confirmed in writing, particularly for fragile or high-value goods.

How does being part of a freight forwarder network in Singapore help me in LCL specifically?

The freight forwarder network in Singapore gives you access to members at destination ports who are already vetted, already operating to the same professional standards you are, and already interested in a reciprocal relationship. X2 Cold Chain is a leading network compiled of dedicated personnel fully versed in their specialist cargo. The same principle applies across X2's networks: members work with members, share rate intelligence, and build the baseload commitment that unlocks better co-loader rates. A single independent forwarder in Singapore cannot commit 200 CBM a month to a co-loader. A coordinated group of network members on a shared lane absolutely can.

When should I advise a client to switch from LCL to FCL?

When your shipment passes roughly 12 to 15 CBM, FCL often becomes cheaper on a per-unit basis than LCL, especially once you factor in local charges and time. A 40-foot container has double the space of a 20-foot but typically costs only about 20 to 25% more. Run the numbers for any client whose LCL volumes are growing. Being the forwarder who tells a client they should actually book a full container, rather than keeping them on LCL because that is what they have always done, earns trust. That trust is harder to price-compete against than any rate you could offer.

Conclusion

Singapore is not going to stop being the LCL hub of Southeast Asia. Singapore continues to serve as an indispensable pillar of global trade, securing its relevance as the primary transhipment and LCL consolidation nexus in Asia by justifying the high operating costs with minimal cost of logistical failure.

Independent forwarders who want to compete in this market do not need to out-volume the MNCs. They need to out-execute them on the things MNCs are structurally bad at: specific lane knowledge, transparent pricing, trusted partner relationships at both ends, and genuine client advisory rather than rate-sheet selling.

Being part of a strong freight forwarder network in Singapore and globally is what makes that execution possible for operators who cannot do it alone. The co-loader relationships, the destination partners, the volume aggregation, the rate intelligence: all of it is more accessible inside a community of forwarders working together than it is for any single independent trying to build it from scratch.

That is what X2 Logistics Networks is built around.

Learn more about membership and how X2 Consolidators supports LCL forwarders at x2logisticsnetworks.com